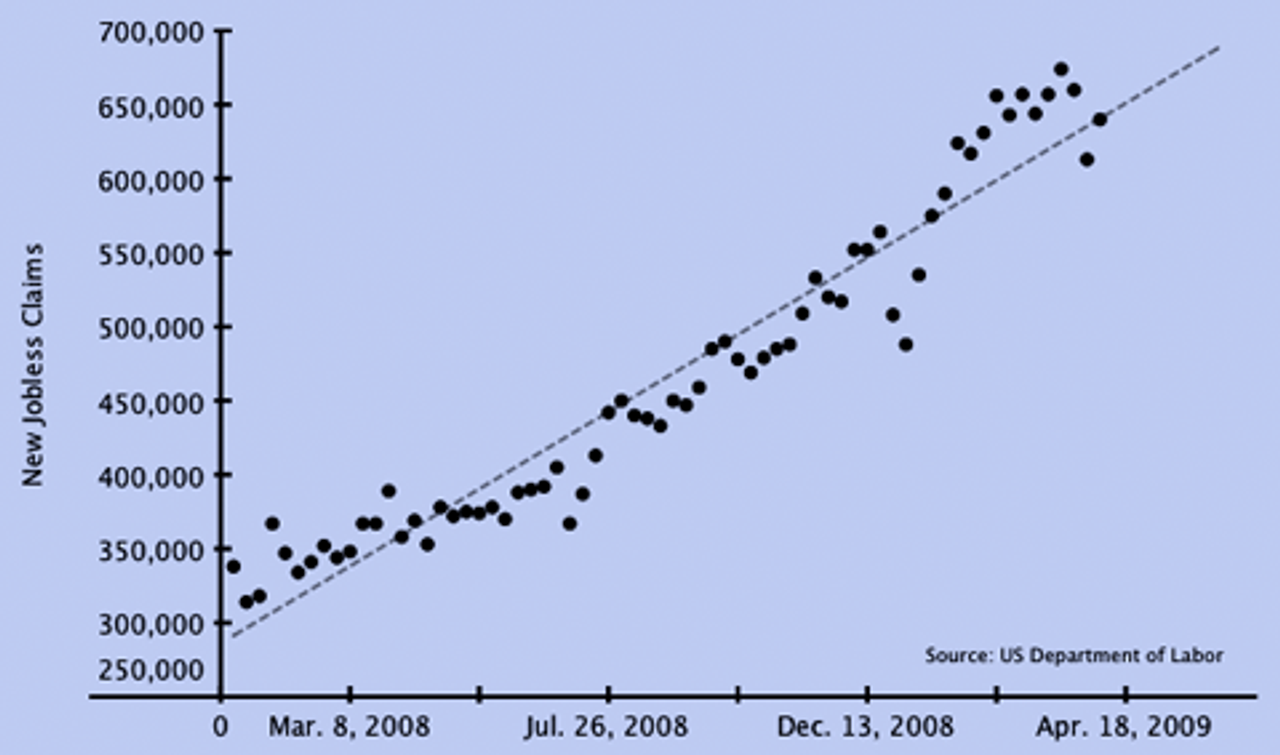

The US Labor Department reported Thursday that there were 640,000 new claims for unemployment compensation last week, up 27,000 from the previous week. The US economy has been hemorrhaging jobs at a rate of well over 600,000 per month since January.

The report noted that the number of people re-applying for unemployment benefits reached 6.13 million, setting a new record for the 12th consecutive week.

New jobless claims

New jobless claims

Also on Thursday, the Labor Department reported that US employers carried out 2,933 mass layoffs in March. Those layoffs eliminated 299,388 jobs. The department defines a mass layoff as affecting at least 50 people.

Nearly half of the mass layoffs were in the manufacturing sector. There were 164 more mass layoffs in March than in the previous month. Compared to March of 2008, mass layoffs have nearly doubled.

Additionally, the Labor Department reported on April 17 that unemployment rates rose in 46 of the 50 states in March. Michigan, wracked by the collapse in the auto industry, again had the highest state unemployment rate at 12.6 percent. It was followed by Oregon with 12.1 percent, South Carolina with 11.4 percent and California with 11.2 percent. The jobless rate in Michigan jumped 0.6 percent from February.

Yahoo announced this week that it would lay off 700 employees in its third set of job cuts since January. Halliburton, the oil contractor, announced that it eliminated 2,000 jobs in the first quarter of this year.

The National Association of Realtors said Thursday that sales of existing homes fell 3 percent in March. Home sales are down by 7.1 percent over the previous year, and housing values have dropped by 12 percent over the same period. The sales decline, higher than projected by economists, followed an unexpected increase of 4.9 percent in February.

The realtors’ organization said that “distressed” home sales, including foreclosed properties, now account for half of all home sales. Such properties typically sold for 20 percent less than other properties.

On Friday, the Commerce Department reported that new home sales fell 0.6 percent to an annual rate of 356,000 in March. That was better than analysts had projected, but still down 30.6 percent compared with the same period a year ago. New home sales in the US have fallen a staggering 74 percent from the peak in July 2005.

Sales fell most sharply in the Northeast, 31 percent, and 7.8 percent in the Midwest. They were unchanged in the South but surged 15 percent in the West, where the housing collapse was the most precipitous. Median new home prices fell to $201,400 compared with $229,300 in March 2008.

Low interest rates, facilitated by the Federal Reserve’s intervention into bond markets, plunging house prices and an $8,000 tax credit for first-time home buyers have not pushed up overall sales. This is, in part, because banks have constricted their lending, and the soaring jobless rate has depressed demand.

Fitch Ratings said this week that it does not expect house values to stop falling until late 2010. It issued a report predicting that house prices will fall another 12.5 percent from the end of 2008, revising its previous projection of a 10 percent decline. US house values have fallen by 27 percent since the housing bubble imploded.

Orders for durable goods in March fell 0.8 percent, the Commerce Department reported Friday. Durable goods are defined as those meant to last several years. The March decline was less than forecast.

But in another sign of deepening slump, the Labor Department reported last week that consumer prices fell by 0.4 percent over the past year to March. This marks the first year that consumer prices dropped since 1955. Prices declined 0.1 percent from February to March of this year.

Most indicators of crisis have surpassed the projections of economists. In mid-2008, Nouriel Roubini, the New York University economist, estimated that bank losses would top $2 trillion. This was among the biggest estimates at the time. It has now been doubled by the International Monetary Fund’s new projection of $4.1 trillion in bank losses, with write-offs in the United States totaling $2.7 trillion.

The economic indicators suggest that the slump is likely to be far deeper than the projections of the Obama administration. The government’s bank “stress tests” assume that, in the most adverse case, the unemployment rate will peak at 10.4 percent in late 2010.

But the unemployment rate hit 8.5 percent last month, and has been rising on average by 0.43 percentage points every month for the past four months. If it continues at this pace, it will hit the government’s outer limit projection in July, over a year ahead of White House estimates.

The Obama administration estimates that its economic stimulus plan will “create or save” 3.5 million jobs. This is equivalent to slightly more than five months’ job losses at current rates.