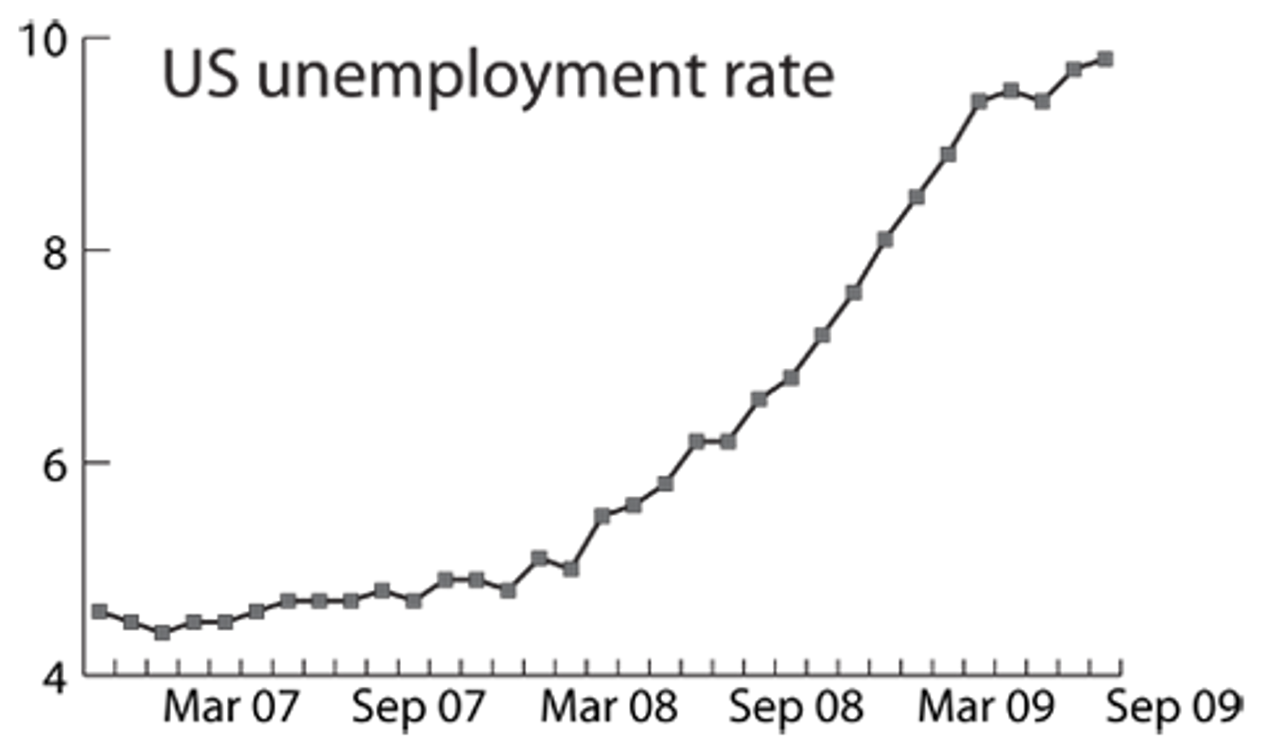

The US unemployment rate reached 9.8 percent and the economy lost 263,000 jobs in September, according to figures released Friday by the Labor Department. The latest figures undermine claims of an imminent economic recovery and point to the likelihood that the US economy will remain mired in recession for the foreseeable future.

The job losses were far higher than predicted. Economists surveyed by Dow Jones newswires expected an average decrease of 175,000 jobs, while the most pessimistic expected no more than 250,000. The job losses for August were revised downward to 201,000. With the new figures, the number of job losses increased by 31 percent from the previous month.

The unemployment rate, which is calculated using separate data, grew by 0.1 percent in September to reach 9.8 percent, up from 6.2 percent in September 2008.

Since the recession started less than two years ago, the ranks of unemployed have swelled from 7.6 million to 15.1 million, while the unemployment rate has doubled.

Long-term unemployment also reached a record high, as the number of people unemployed for 27 weeks or more has increased by 260 percent over the previous year. In September 2008, there were 2 million people considered “long-term” unemployed, but last month this figure jumped to 5.4 million, representing 35.6 percent of unemployed people. The average duration of unemployment has hit a high of 26 weeks this month.

The labor force participation rate fell by 0.3 percent over the previous month, as more workers became discouraged by dire employment prospects. On September 26, the Labor Department reported that there are now six job seekers for every permanent job opening, up from a ratio of about two to one a year ago.

Each of the Labor Department’s measures for unemployment increased in September. The broadest measure, including discouraged workers and people forced to work part time, reached 17 percent last month. This is up from 16.8 percent in August and 10.6 percent a year ago.

The sectors with the largest number of job losses were manufacturing, construction, retail and government. Manufacturing lost 51,000 jobs, roughly in line with the past three months. The sector has lost 2.1 million jobs since the recession started in 2007. The retail sector lost 39,000 jobs, while construction lost 64,000.

The government sector lost 53,000 jobs, nearly half of which were in state and local government. This loss is largely attributable to the state budget crises, which have forced states and municipalities to trim their payrolls as tax revenues plummet.

Auto dealerships cut 7,100 jobs in September as the government’s “cash for clunkers” program expired. Car dealers added jobs in August in response to the government’s program, which offered consumers thousands of dollars in incentives to buy new cars. Auto sales plunged by 23 percent following the end of the program.

Meanwhile, the average workweek fell 0.1 hours to a record low of 33.0 hours, and overtime decreased by the same amount. Temporary employment agencies, which typically respond quickly to economic upturns, cut 1,700 jobs.

Factory goods order figures released Friday by the Commerce Department are equally grim. The figure fell in August by 0.8 percent, higher than Wall Street’s prediction of 0.6 percent, and significantly lower than the previous month’s increase of 1.4 percent. Durable goods orders, meanwhile, fell by 2.4 percent in August. Similarly, the Institute for Supply Management reported Thursday that its index of manufacturing activity fell from 52.9 to 52.6 in September.

On the consumer side, the Confidence Board’s index of consumer sentiment fell to 53.1 last month, down from 54.5 in August, according to figures released Tuesday.

Meanwhile, the number of home foreclosures rose by 17 percent in the second quarter, according to figures released Wednesday by the Office of Thrift Supervision. There were 106,007 foreclosures in the second quarter, compared to 90,696 in the first quarter.

The latest figures offer an indication of just how deeply mired the United States is in the longest recession in the country’s postwar history. Despite claims of imminent “recovery,” including from Obama and Federal Reserve Chairman Ben Bernanke, there is near-universal acceptance that hundreds of thousands more people will lose their jobs before the recession is over, and that large numbers of people are likely to stay unemployed for years to come.

Indeed, there is near-universal acceptance that, nominal recovery or not, there will be further widespread suffering among workers. Paul Krugman pointed out Friday that, by the Obama Administration’s own estimate, “the unemployment rate, which was below 5 percent just two years ago, will average 9.8 percent in 2010, 8.6 percent in 2011, and 7.7 percent in 2012.” In a similar vein, Ben Bernanke said that, even if the economy returns to an unlikely 3 percent growth rate next year, the unemployment rate would likely remain above nine percent by the end of the year.

One year since the start of the bank bailout, the policy of the ruling class has borne its fruit: wages are falling, unemployment creeps upward, and every indicator of social misery is approaching its postwar high. But the big banks are seeing profits return.

Despite some recent losses, the US stock market is in the midst of a significant rally. Over six months, the Dow Jones Industrial Average is up by 18.34 percent, the S&P 500 is up by 21.69 percent, and the NASDAQ is up by 26.28 percent.