The following article is based on a report given by Peter Schwarz, secretary of the International Committee of the Fourth International, at a seminar of the German section of the Socialist Equality Party during the Easter holidays in 2011. Part 1 was published on May 30, 2011.

The crisis of the European Union

The differences between Germany and France are not limited to matters of foreign policy. Sharp conflicts also exist in economic and financial matters, which are endangering the euro and the European Union itself.

The introduction of the euro did not, as Helmut Kohl, Joschka Fischer and others had expected, lead to greater harmony in Europe. Instead it intensified economic and social differences. A large amount of statistical material shows that the growing conflicts between Germany and France and the fracturing of the EU are by no means accidental.

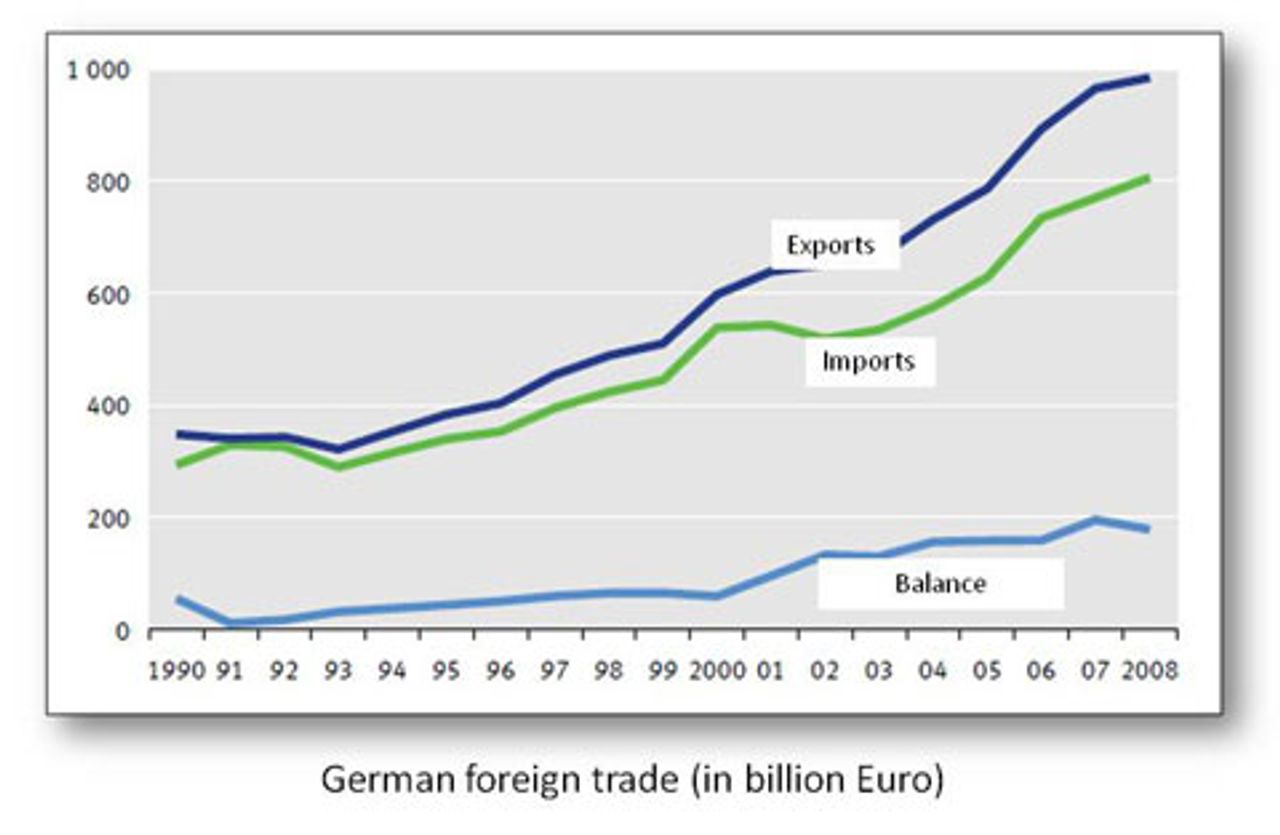

The German economy has benefited greatly from the introduction of the euro. Between 1990, the year of German unification, and 2008, German exports have almost tripled: from €348 billion to €984 billion. Imports have also grown considerably: from €293 billion to €806 billion.

Of particular importance is the increase of the surplus in foreign trade. It has more than tripled between 1990 and 2008. It initially went down after the re-unification. The German economy at that time was more focused on domestic than foreign trade. But during the 1990s the surplus in foreign trade increased continually. The biggest leap was between 2000 and 2005, when it rose by 22 percent a year. In 2007 it reached the record value of €200 billion.

Basically, three factors contributed to the increase in German exports and in the surplus in foreign trade–the introduction of the euro, EU enlargement into Eastern Europe, and the development of the low-wage sector caused by the Agenda 2010 reforms.

The euro protected Germany against currency fluctuations within Europe and maintained the currency at a relatively low value internationally, thereby strengthening Germany’s export industry in Europe and internationally.

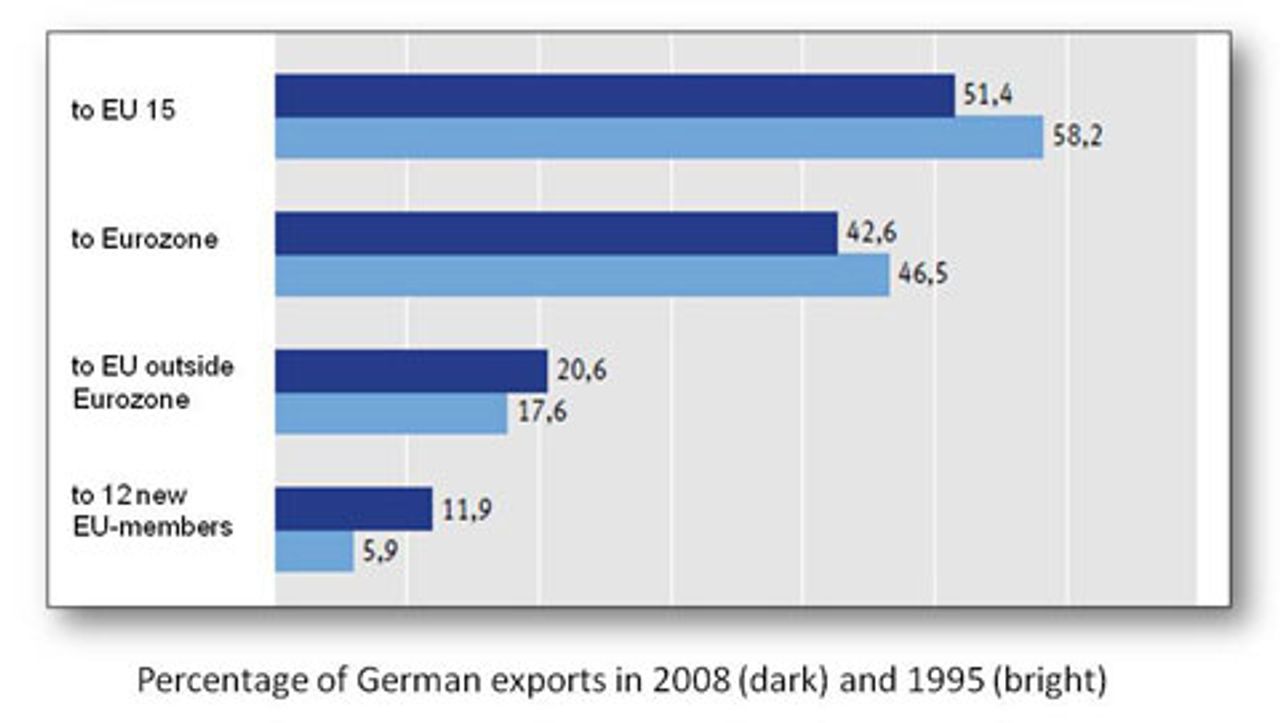

In 2008, 63 percent of the German exports went to EU countries and 43 percent to members of the Eurozone. Two thirds of the exports were paid in euros, thus making them independent of currency fluctuations.

Through the euro, Germany’s currency was artificially kept low. Had European countries maintained their national currencies, then the deutschmark would have risen sharply against inflationary currencies such as the Greek drachma, the Italian lira and the French franc. It probably would have also risen against the US dollar and the Japanese yen. With the introduction of the euro, however, currency relations remained stable.

While prices and nominal wages rose in weaker European countries after the introduction of the euro, they barely increased in Germany. This was mainly due to the Schröder administration’s Agenda 2010, which created a huge low-wage sector and significantly depressed wages, and was introduced with the support of the unions.

Consequently, during 2000 and 2010, unit labour costs in Germany rose less than in the rest of Europe. In Germany, they only increased by 0.7 percent annually, while the EU average was 2.1 percent. In Greece, they rose by 3 percent, in Portugal by 2.7 percent and in Spain by 2.6 percent annually. In France they also rose by 1.9 percent a year, more than twice as fast as in Germany.

The consequence was a dramatic increase in economic imbalances in Europe. While Germany’s foreign trade ran a surplus, deficits grew in France and Great Britain. Measured against its GDP, Germany’s foreign trade surplus in 2008 was 7.1 percent. France recorded a deficit of 3.5 percent, Great Britain a 6.6 percent deficit and Poland a deficit of 6.8 percent.

Germany also benefited from the eastern enlargement of the EU. While the share of its exports into the older EU states decreased significantly, German exports into the new member states doubled. These countries also functioned as an extended production line for Germany. Foreign trade statistics not only include exports of finished products such as cars and machines, but also so-called “intra firm trade”. If goods pass borders several times during their manufacturing process, this “globalization effect” is noted in the statistics, and artificially inflates them.

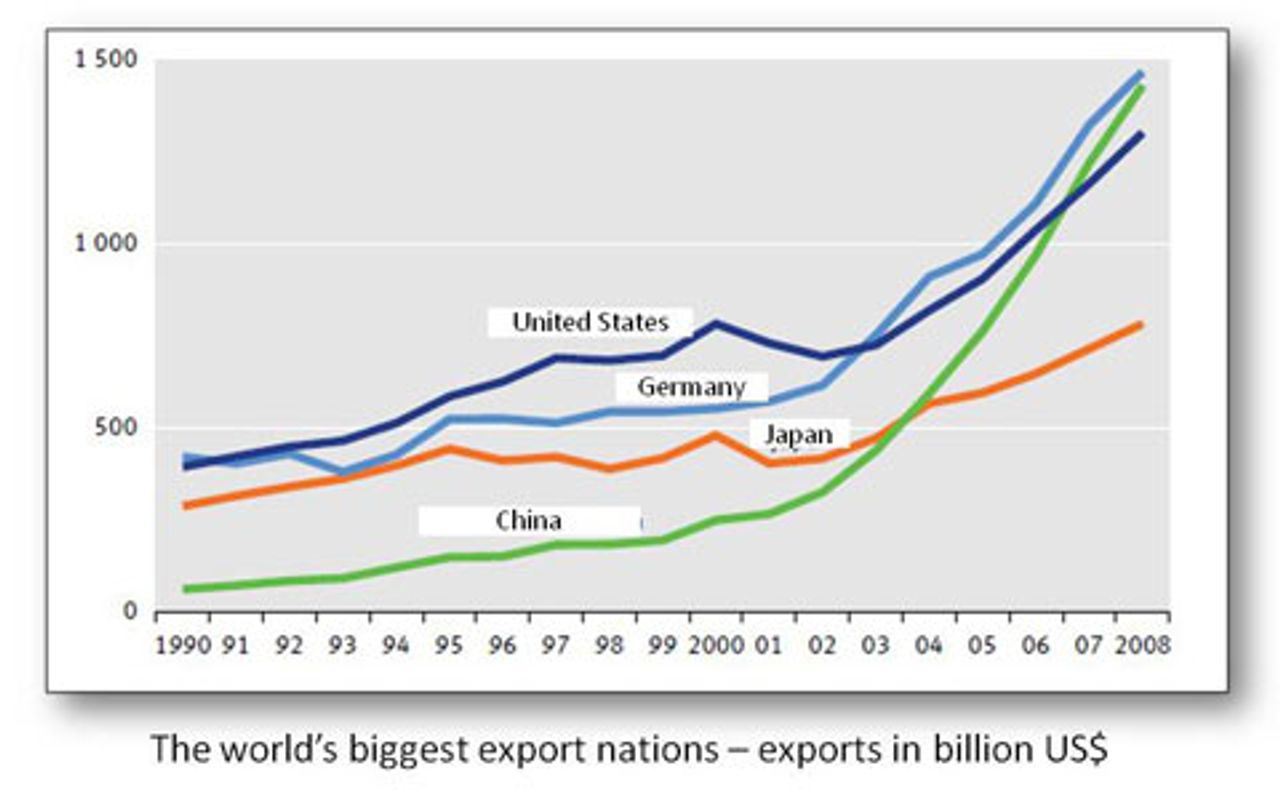

The past 20 years have witnessed a considerable shift in terms of international trade not only in Europe, but also globally. Germany has surpassed the US in terms of exports, while Japan has fallen back sharply. However, the real front-runner is China, whose exports have risen from $62 billion in 1990 to $1.4 trillion in 2008, a 22-fold increase.

Another important criterion for international economic relations is Foreign Direct Investment (FDI). The OECD defines it as follows: “FDI is defined as investment by a resident entity in one economy that reflects the objective of obtaining a lasting interest in an enterprise resident in another economy”.

In other words, its aim is to exploit workers of foreign countries via the mechanism of capital export. Already Lenin had identified capital export an important feature of imperialism. He wrote, “Typical of the old capitalism, when free competition held undivided sway, was the export of goods. Typical of the latest stage of capitalism, when monopolies rule, is the export of capital”.

During the last two decades, there has also been a considerable shift in this sector. On the basis of its high export surplus, Germany has become an important capital exporter. Since 1990, German capital investment in foreign countries has grown six-fold, while foreign capital investment in Germany has risen four-fold.

However, as a percentage of GDP, as well as in absolute figures, the former European colonial powers of Great Britain and France continue to outstrip Germany in the field of FDI.

In 2008, the UK’s Foreign Direct Investment was 57 percent of its GDP. This puts the UK before France (50 percent) and Germany (40 percent). In absolute figures, the UK’s FDI were €1.8 trillion, compared to France, €1.3 trillion and Germany, €1.2 trillion. First place went to the US with €3.5 trillion.

German FDI was concentrated mainly in Europe and the US. In 2004, 50 percent was invested in the old EU states and 30 percent in the US. Some 6 percent were invested in the new EU members, and only 1 percent in China.

To be continued