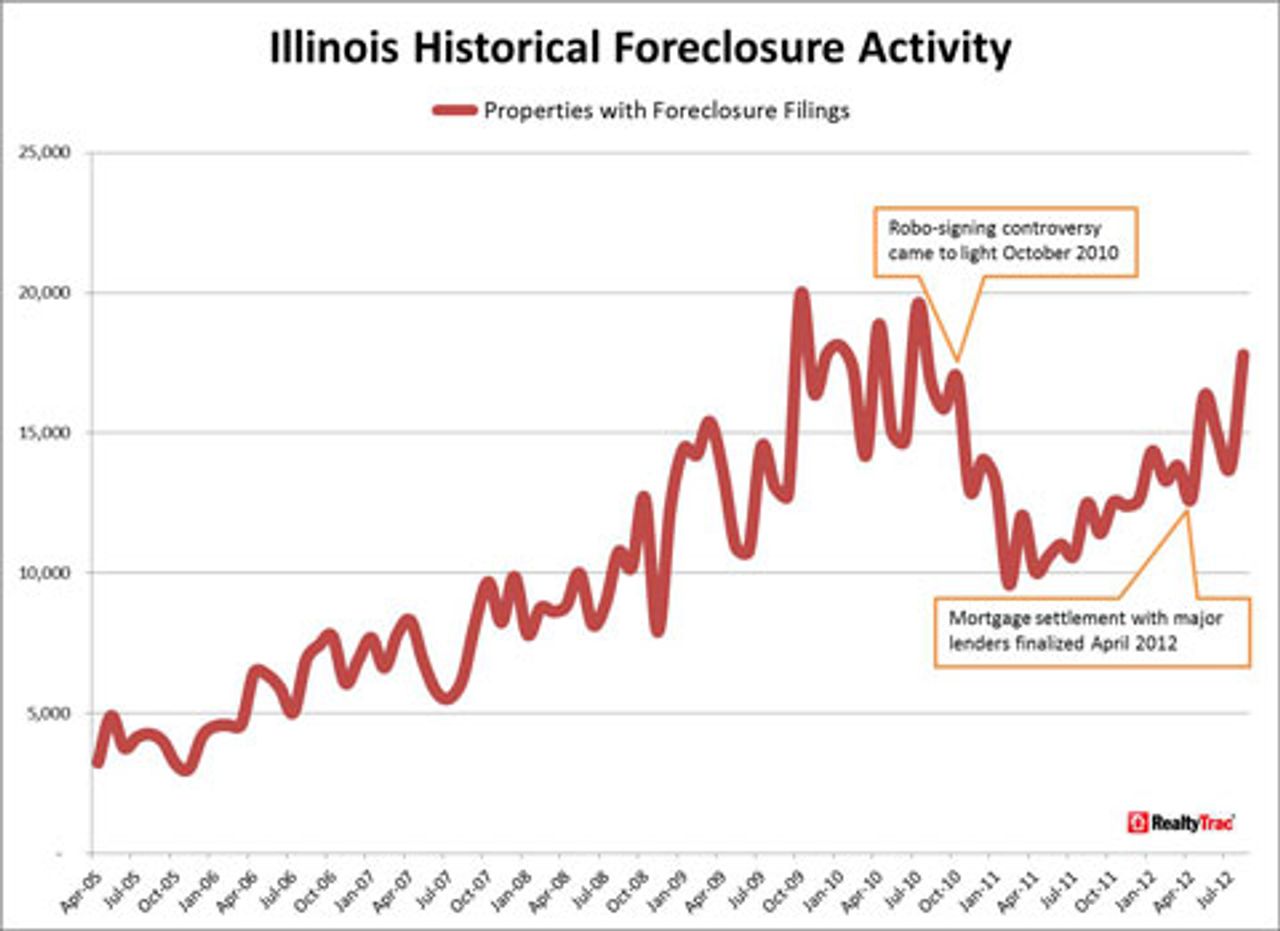

Foreclosure activity in Illinois jumped 29 percent between July and August and was up 42 percent from a year ago, giving the state the highest foreclosure rate in the US, according to the latest report from foreclosure tracking firm RealtyTrac. This marks the first time Illinois has had the nation’s highest rate since RealtyTrac began publishing monthly reports at the start of 2005.

As of August, 1 in every 298 housing units in Illinois had a foreclosure filing, more than double the national rate of 1 in 681. RealtyTrac noted that every kind of foreclosure activity had increased on annual basis in Illinois: foreclosure starts by 18 percent, bank repossessions by 42 percent, and scheduled foreclosure auctions by 116 percent.

Daren Blomquist, vice president of RealtyTrac, told Bloomberg’s Businessweek that foreclosure filings in Illinois will likely increase every month for the rest of 2012 and exceed the previous high set in 2009. “More Illinois homeowners are entering the foreclosure process, and more are losing their homes,” he said. “It’s going to get worse before it gets better.”

According to Businessweek, the high number of foreclosures is now luring investors to Illinois’s real estate market. Large private equity firms are expecting returns of as much as 20 percent from the purchase of repossessed homes, which are subsequently offered as rental properties.

The article described these predatory practices: “Waypoint Real Estate began acquiring steeply discounted Chicago foreclosures two months ago after amassing about 2,000 distressed homes in California since January, 2009, Gary Beasley, managing director, said in a telephone interview. Waypoint has also been buying foreclosures in Arizona since April, and generally acquires properties that have lost half their value, he said.”

Chicago’s foreclosed homes sell at approximately $130,000, on average, which is the third lowest value among America’s top 20 cities. Nationally, the average price for a foreclosed home is $170,000. The article additionally noted that foreclosed properties on the south side of Chicago can be had for less than $20,000, “all in cash.”

The Chicago metro area had more new foreclosure filings in August than any other city in the US, and these 16,192 filings accounted for 91 percent of the total new filings in Illinois. Filings increased in the city by 28 percent from July and by 44 percent from a year ago.

Property values in Chicago have dropped 8 percent so far this year, and more than 5 percent across the state of Illinois, according to Zillow.com. The destruction of home equity in the ongoing mortgage crisis has left families going through foreclosure with zero wealth, as most working people in the US invested what they had in their homes.

In addition to Chicago leading the nation in the overall number of foreclosure filings, it also outdistanced the rest of Illinois in its foreclosure rate, which, at 1 in 235, was nearly triple the national rate.

Rockford, Illinois, also had one of the top 10 metropolitan area foreclosure rates nationally, with 1 in 259 housing units in the foreclosure process. Rockford saw an even larger year-over-year increase than Chicago and the state overall, at 52 percent.

Belying claims of an overall recovery in the housing market, nationally foreclosure filings were issued on a total of 193,508 homes in August, marking an increase of 1 percent from July. Twenty states saw increases in foreclosure activity compared to August 2011.

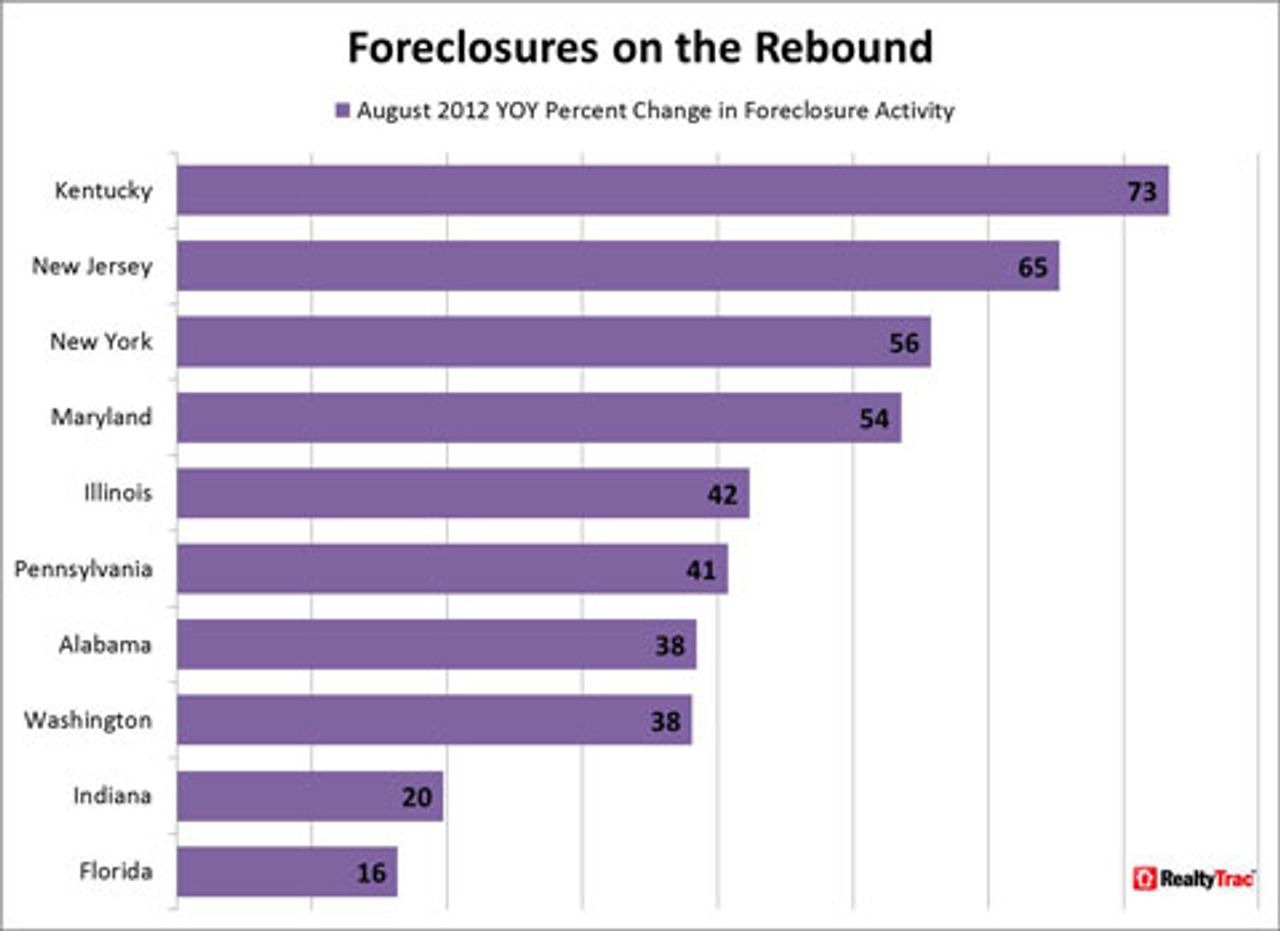

Although Illinois led the nation in foreclosure activity last month, four other states actually saw even sharper year-over-year percentage increases in their foreclosure activity. They included Maryland, with a 54 percent increase; New York, with 56 percent; New Jersey, with 65 percent; and Kentucky, with a 73 percent increase.

As the WSWS has noted previously, the surge in home foreclosures is no accident. When allegations of mortgage fraud and “robo-signing” first emerged against the major banks in 2010, foreclosure activity briefly subsided under the scrutiny of a number of state investigations.

However, last February, the Obama administration once again rose to the defense of its financial backers when it orchestrated a settlement that shut down state investigations and required mortgage lenders to pay a pathetically small cash fine. More importantly, the agreement cleared lenders of any wrongdoing in relation to the scandal and prevented any future prosecution. Since then, foreclosure activity has surged in numerous states as the banks have moved to clear their books of any remaining bad debt.

Despite the parlous state of the housing industry and its devastating consequences for working families, a brisk business is still being turned at the real estate market’s upper reaches.

In a recent article in the Chicago Tribune, Craig Hogan, director of Coldwell Bankers Preview, estimated that so-called superluxury buyers will only look at properties valued above $3 million and typically pay 50 percent of the asking price in cash. “Upper-bracket buyers want showplaces, trophy mansions, ego enhancers. Their house is their calling card and it must make a statement. They want the best of the best, the best finishes, everything world-class and cutting edge.”

Sara Benson, president of Benson Stanley Realty, added, “The rich like to reside among their peers on a mansion row, or in condos and co-ops with compelling views. The wealthy like one-of-a-kind spaces.” Condos at Trump Tower in downtown Chicago, for example, range in price from $3 million for a 3,000-square-foot unit to $32 million for the 89th floor penthouse, which offers “360-degree views of the lake and city.”

The author also recommends:

Statement by Jerry White, Socialist Equality Party candidate for US president:

For a socialist program to stop foreclosures!

[2 August 2012]