Below we are publishing the first part of the opening report given by Nick Beams to an international school held by the International Committee of the Fourth International (ICFI) and the International Students for Social Equality (ISSE) in Sydney, Australia from January 21 to January 25. Beams is a member of the international editorial board of the World Socialist Web Site and the national secretary of the Socialist Equality Party of Australia.

The second part of the report will be posted on February 1.

At our school ten years ago, held on the eve of the launching of the World Socialist Web Site, we spent some time examining the implications of the so-called Asian financial crisis which had erupted the previous July.

In delivering a report on this crisis, I said it was somewhat difficult because we were confronting a moving target. Today, I have the feeling of déjà vu in the midst of what is undoubtedly a deepening crisis of American and world capitalism.

When the Asian crisis erupted, we explained that it was not so much an Asian crisis as a crisis of world capitalism which had manifested itself in Asia. Today, we are confronted not simply with the crisis of American capitalism, but a world crisis which has erupted in the United States.

Every day brings further news of losses by the major finance houses—Merrill Lynch has just suffered write-offs of $16.7 billion—and warnings that more are to come. Citigroup has just announced its biggest loss in its 196-year history—$9.83 billion for the last quarter—after writing down the value of subprime mortgage investments by $18 billion.

Major financial institutions are scrambling to ensure large injections of cash from anywhere they can find them—Merrill Lynch and Citigroup alone are trying to raise $21 billion from funds in Singapore and Saudi Arabia.

Each day brings new announcements. The Economist of January 18, under the headline “All Fall Down?”, reported on the developing crisis within the bond insurance market. It wrote:

“America’s big bond insurers, which have underwritten some $2.4 trillion of private and public-sector bonds, usually go about their business largely unnoticed. But now they are looking distinctly wobbly they have started to attract attention. If one or more of them were to topple over, there will be a huge knock-on effect on banks and other financial institutions that rely on their guarantees. This in turn will further worsen the credit crunch and cause an even bigger headache for policymakers already grappling with a sharp slowdown in the American economy.

“The threat of such a financial domino effect looms large. Moody’s, a credit-rating agency, has signalled that it might downgrade the AAA ratings of two of the biggest bond insurers, MBIA and Ambac, in the near future.”

On January 16, Ambac announced a $3.5 billion writedown, as well as the ousting of its chief executive. The Economist quoted Jamie Dimon, the boss of JP Morgan Chase, who said that the fallout from the bond-insurer crisis could be “pretty terrible” for the debt markets. The magazine commented that “if a big insurer... were to take a tumble, that could look like an understatement.”

Most economists are now predicting a recession and discussion is centring on how soon it will come and how long it will last.

On January 10, Federal Reserve Board Chairman Ben Bernanke delivered a major speech on the US economy in which he all but guaranteed a significant further cut in interest rates when the Fed’s open market committee next meets at the end of the month. But instead of this news providing a lift to financial markets, the Dow Jones Industrial Average fell 250 points following the speech.

Little wonder. Bernanke spoke of a “volatile situation that has made forecasting the course of the economy even more difficult than usual,” pointed to the fall in home starts and new home sales of about 50 percent from their respective highs, noted the “considerable investor uncertainty about the appropriate valuations of a broader range of financial assets, not just subprime mortgages,” warned that “incoming information has suggested that the baseline outlook for real activity in 2008 has worsened and the downside risks to growth have become more pronounced,” and said that despite improvements in some areas “the financial situation remains fragile.”

Just how fragile can be seen from the comments which have appeared in the financial press over the past couple of months.

The Economist noted on December 19 that the crisis is more than a liquidity squeeze, but “now looks like becoming a banking crisis as well.” The “stomach-churning moment” came last November when it was realised that the losses from the housing market would be big, the banks would end up taking them, and that they had not put capital aside to meet them. “Bankruptcies, recession, litigation, protectionism: sadly, all are possible in 2008,” it warned.

In a column published on December 12, Financial Times economics commentator Martin Wolf wrote: “First and foremost, what is happening in credit markets today is a huge blow to the credibility of the Anglo-Saxon model of transactions-orientated financial capitalism. A mixture of crony capitalism and gross incompetence has been on display in the core financial markets of New York and London.”

David Ignatius wrote in the Washington Post of December 16: “The global credit squeeze that began last summer still hasn’t run its course, and the central bankers fear that the stressed financial system will pull the world economy into deep recession.”

Financial Times columnist Wolfgang Munchau made the point in a comment on December 16 that the crisis is not a liquidity crisis at its core because if it were it would be over by now.

“It is,” he wrote, “a fully fledged solvency crisis that has arisen because two giant and interlinked bubbles burst simultaneously—one in property, one in credit—leaving banks and investors on the brink of bankruptcy, some hanging on by their fingertips. Yet there is nothing the central banks are offering at this stage to alleviate a solvency crisis.”

Comments by Bill Gross, the head of Pimco asset management group, were quoted in sections of the financial press. “What we are witnessing,” he said, “is essentially the breakdown of our modern-day banking system, a complex of leveraged lending [that is] so hard to understand.” Pimco is no small operation, managing about $1 trillion in funds.

The first signs of the crisis emerged in 2006 as housing prices in the US began to turn down. The rapid escalation of financial operations based on mortgages meant that this downturn was of some significance for the financial system and the broader US economy.

The official position of the Fed was that the problems could be contained. On February 14, 2007, Chairman Bernanke noted that “some tentative signs of stabilisation have recently appeared in the housing market.” Then, on March 28, he said, “[T]he impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.”

On May 17, he stated, “We believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spill-over... to the rest of the economy or to the financial system.” On June 5, shortly before the credit squeeze hit, he said, “Fundamental factors—including solid growth in incomes and relatively low mortgage rates—should ultimately support the demand for housing, and at this point the troubles in the subprime sector seem unlikely to seriously spill over to the broader economy or the financial system.”

How far these statements underestimated the situation would soon become clear. In mid-June the subprime crisis began to come into view when the investment bank Bear Stearns announced that two hedge funds it had set up were experiencing problems because of their investments in subprime mortgage debt.

Over the next two months the crisis was to rapidly unfold as concerns grew over the extent of involvement of major banks and financial institutions in risky financial operations. On August 17, the US Federal Reserve made its first major intervention, announcing a cut in the discount rate charged to banks. This followed a roller coaster day on Wall Street in which there were two major interventions by financial authorities to prevent a plunge. It was clear that without an intervention by the Fed, the market could have plunged by up to 1,000 points the following day.

The Fed again moved on September 18, cutting the federal funds rate by 50 basis points. This brought some relief to the markets, but by November it was clear that the crisis was far from over.

The basic problem was that the fundamental credit operations of the global capitalist system were being affected by a collapse of confidence. Major banks and financial institutions were refusing to lend either because they wanted to keep cash on hand in case some of their own off-balance-sheet operations started to fail or because they did not know the extent of the exposure to doubtful debt of the banks and other institutions to which they might lend.

These fears were reflected in the movements of the LIBOR rate (the London Interbank Offered Rate), the rate at which banks will make unsecured loans to other banks. In normal times, LIBOR is marginally higher than the interest rate on US treasuries, regarded as the safest form of investment. But as the subprime crisis broke and as the write-downs by major banks grew, so the LIBOR rate rose sharply.

Sharp increases in the LIBOR rate reflect the lack of confidence the major banks—the top names and institutions in the financial world—have in one another. This lack of confidence is magnified when it comes to other financial institutions. They have found that the cheap money that was once available to them, and on which they have based their operations, is no longer available.

This is what led to the demise of the Northern Rock Bank in England. It was not made bankrupt because it had invested in US subprime mortgages—its involvement in this area was negligible. Rather, it fell victim to the credit crunch which was set off by the subprime crisis.

Northern Rock made its money by borrowing in the short-term credit markets and then using this cash to finance long-term loans, at slightly better rates than those offered by other financial institutions. Operating on narrow margins, it had to borrow large amounts of money. This method worked well... so long as the short-term credit was continuously available. But when it was not, the bank collapsed.

The same process has brought down the Australian property group Centro. For the past decade it had produced annual returns to investors of more than 20 percent a year on a strategy which involved buying up shopping centres in a rising market and then selling off part of each centre to managed funds. Last May it made its biggest deal, a transaction of $6.3 billion in the United States. It chose to fund part of the deal with short-term credit.

On December 17, it announced that it could not refinance $2.5 billion worth of short-term debts. According to the Centro chairman: “We never expected, nor could reasonably anticipate, that the sources of funding that historically have been available to us and many other companies would shut for business.”

As has so often been the case in the past, the financial crisis has struck the world economy right at the point where it was experiencing a major upswing.

Last May, the International Monetary Fund’s “World Economic Outlook” (WEO) noted that the average world growth rate for the period 2003-2006 was 4.9 percent and predicted it would continue for at least the next two years. The only stronger spurt was the period 1970-1973, when world growth averaged 5.4 percent. If the current rate were sustained, the IMF report explained, it would represent the most powerful six-year expansion of the world economy since the 1970s.

The picture painted by the “Global Economic Prospects” report published by the World Bank in December 2006 was not essentially different. It pointed to a “strong global performance,” reflecting a “very rapid expansion in developing countries, which grew more than twice as fast as the advanced economies.” This was not just a result of the impact of the Chinese economy, which grew by 10.4 percent, but extended across the range of developing countries. Altogether, 38 percent of the increase in global output originated in these regions, well above their 22 percent of world gross domestic product (GDP).

The World Bank report noted that if the past 25 years were divided in two periods—1980-2000 and 2000-2005—average growth in developing countries had accelerated from 3.2 percent in the first period to 5 percent in the second. While this acceleration was not shared by all countries, neither was it merely the result of increased growth in China and India.

The IMF’s WEO report was filled with similar stories of economic success. Economic activity in Western Europe had “gathered momentum” in 2006, with GDP growth in the euro area reaching 2.6 percent, almost double the rate for 2005 and the highest figure since 2000. The report declared: “Germany was the principal locomotive, fueled by robust export growth and strong investment generated by the major improvement in competitiveness and corporate health in recent years.” Overall, the unemployment rate had fallen to 7.6 percent in the euro area, its lowest level for 15 years.

There was even good news from Japan, where the economy was virtually stagnant for more than a decade following the collapse of the share market and land bubble in the early 1990s. Despite an unexpected decline in consumption in the middle of 2006, the “economy’s underlying momentum remains robust, with private investment expanding—supported by strong profits, improved corporate balance sheets, and the resumption of bank lending—and rising export growth.” Real economic growth in Japan was expected to remain at above 2 percent.

While the growth rate in Latin America was expected to ease to 4.9 percent in 2007 from 5.5 percent in 2006, the years 2004-2006 were “the strongest three-year period of growth in Latin America since the late 1970s.”

In so-called “emerging Asia” economic activity “continues to expand at a brisk pace,” supported by “very strong growth in both China and India.” In China, real GDP expanded by 10.7 percent in 2006, while in India the growth rate was 9.2 percent, the result of increased consumption, investment and exports.

Growth in Eastern Europe accelerated to 6 percent in 2006, while in Russia the growth rate of 7.7 percent in 2006 was expected to ease only slightly to 7.0 percent in 2007 and 6.4 percent in 2008.

The WEO report described the economic outlook for Africa as “very positive” against a backdrop of strong global growth, increased capital inflows, rising oil production in a number of countries and increased demand for non-fuel commodities. “Real GDP growth,” the IMF wrote, “is expected to accelerate to 6.2 percent this year (2007) from 5.5 percent in 2006, before slowing to 5.8 percent in 2008.”

The Bank for International Settlements in a report published last June noted that in 2006 total world output had expanded at a rate of 5.5 percent, marking the fourth consecutive year of growth above 4 percent. Economic strength was more broadly based, with virtually all advanced industrial countries growing at above-trend in 2006 and all major emerging markets advancing.

The report stated: “The upswing of the past four years has differed in several respects from that of 1994-97, when the global economy also recorded four consecutive years of growth at or above trend. First, emerging market economies, especially in Asia, have contributed 1.25 percentage points more to global growth than they did a decade ago. To an important extent, this reflects the buoyancy of the Chinese economy.”

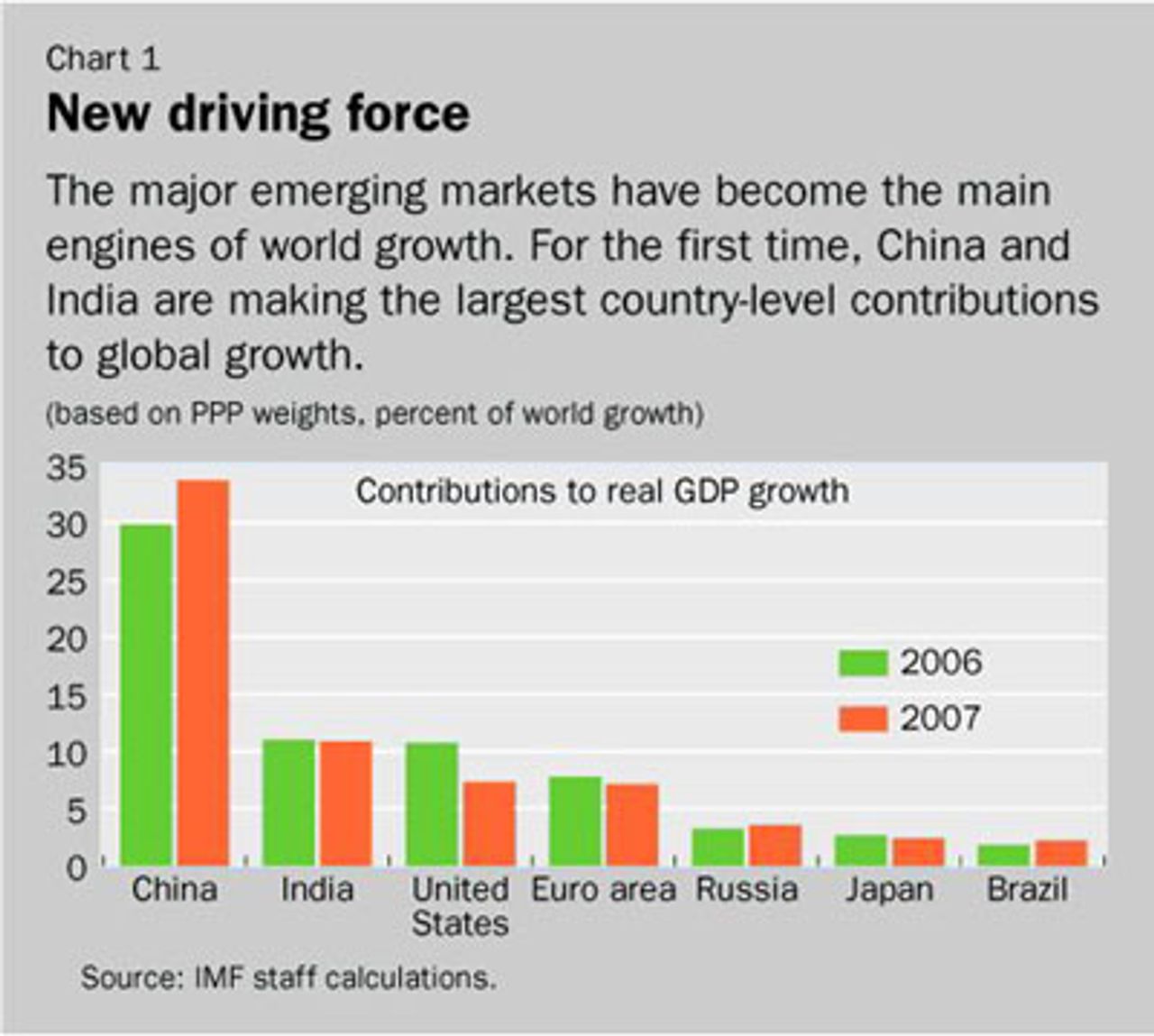

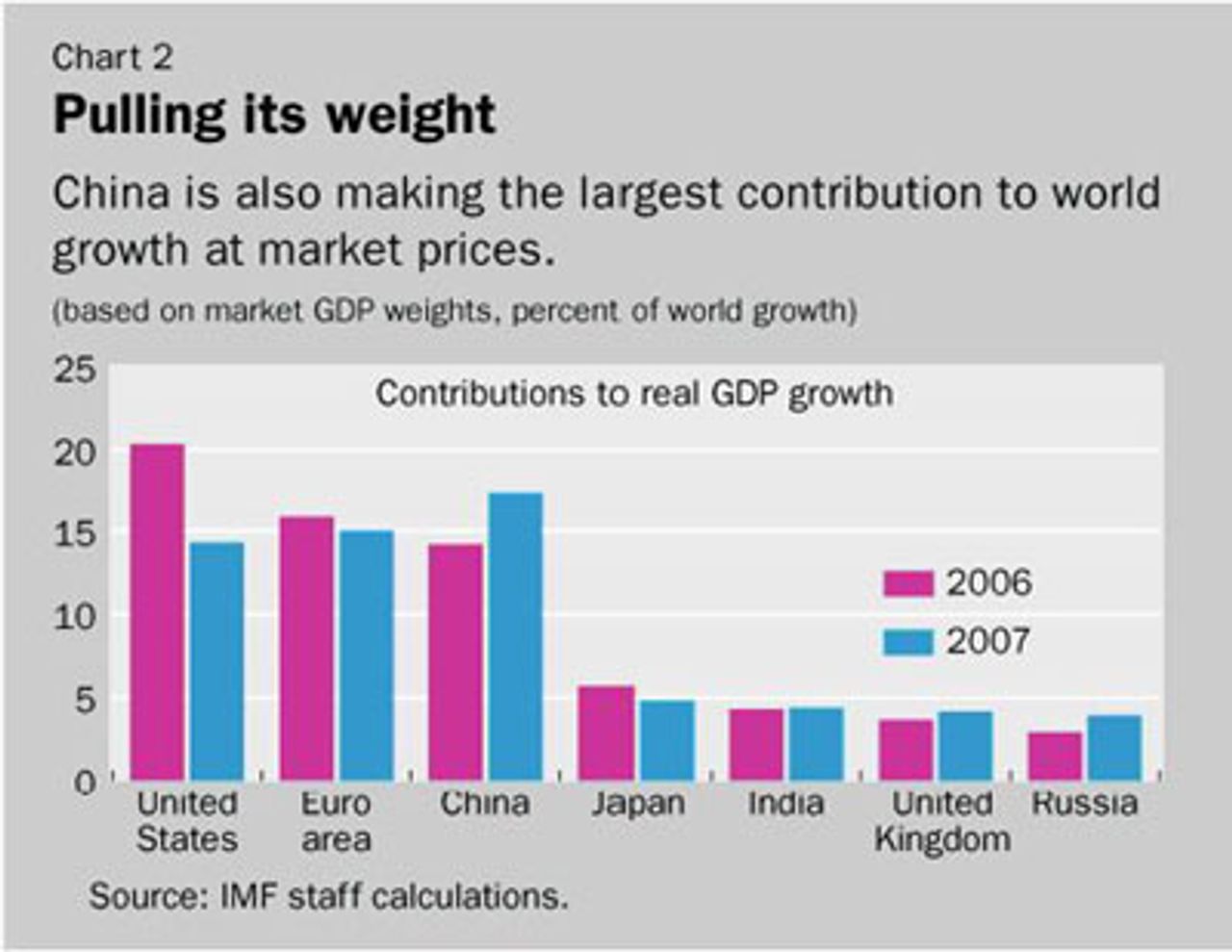

An article published in the IMF Survey magazine of October 2007 makes clear how significant Chinese and Indian economic growth has been. China is now the single most important contributor to world economic growth as the following charts indicate.

(Market exchange rates are those prevailing in the foreign exchange market, while the PPP exchange rate is defined as the rate at which the currency of one country needs to be converted into that of another country so as to be able to purchase the same amount of goods and services in each country. Use of PPP exchange rates gives a greater weight to emerging market economies in the global growth aggregates).

The extent of economic growth in China is summed up in the following amazing statistic: in 2007 China had 7,000 steel factories, double the number it had in 2002.

Financial institutions were also upbeat. In April 2006, Deutsche Bank Research noted that the world economy was enjoying its longest period of growth since the 1970s, but this time without rising inflation. There had been difficulties with New Economy 1.0 in 1999/2000 (the collapse of the share market and dot.com bubble and the development of recession in the US) but “New Economy 2.0 seems to be getting it right now.”

Today the predictions are still that the world economy as a whole will keep growing. In its latest report published last month, the World Bank forecasts that global growth in 2008 will be 3.3 percent, as “the robust expansion in developing countries partly compensates for weaker results in high-income countries.” However, it is not completely sure, adding that “serious downside risks cast a shadow over this soft landing.”

The central question, however, is not whether the US and the world economy as a whole go into recession, but what the processes are that have led to this crisis, and what are their implications.

Here it is necessary to reject the on-the-one-hand-on-the-other approach which characterises the latest World Bank forecast and which will, no doubt, be duplicated elsewhere.

To be continued